Kraken Robotics (PNG-CAN)

The right way to play the intersection of defence & tech

Foreword

I like the intersection and defence and tech - Kraken is one of my favourites from this bunch. Apologies in advance for the text-heavy post. The devil is really in the detail with a growth stock like this

SP: ~3.00 M/C ~C$900m

TD;LR

Specialised manufacturer of subsea battery housing

Emergence of subsea drones provides growth runway

Canadian smallcap w/ little coverage

$7-$8/stock in 2029 - >25% IRR from here.

Business: Unmanned Underwater Vehicles (‘UUVs’). Remotely controlled. The Naval answer to drones. Between 5-10m length, they’re used for minehunting, patrols and will soon be cable of carrying munitions payloads.

Trying to outcompete the Chinese in manufacturing submarines is a zero-sum game. It was 8-10 years for the US to build a Collins-class sub. The argument about UUVs has shifted from if to when. In 2018 the Pentagon released a paper outlining technology as the key to beating China.

Kraken’s key product is subsea batteries. This is specially manufactured silicon housing applied to standard li-on batteries that increases the energy density and therefore the amount of time a UUV can operate without surfacing.

At 6000m depth, water pressure is ~600 bar, crushing electronics. Traditionally, subsea vessels used oil-filled housing to balance the hydrostatic environment. Oil is densely packed at the molecular level – it does not compress very much at depth. Oil-filled housing has a piston system that regulates the volume of oil, equalizing pressure – the same way divers do.

Oil-filled systems require a lot of support structures to handle thermal stresses. The piston system is made of titanium & steel, weighing a lot and creating parasitic mess.

Kraken use a thermally cured silicon matrix. The silicon structure is inherently pressure tolerant itself. This saves a lot of space. A Kraken system requires ~50% less volume to achieve to store the same energy. This means you can pack more energy density into fewer space meaning a UUV requires recharges much fewer. It also saves hull space for sonars and munitions payloads.

The customer value unlock is utterly massive – you can charge a lot. Particularly when there is no competition. You can charge like a wounded bull because the end-customer is the Military. Despite this being a capital good (most buyers negotiate the price of a capital good) - there is unlikely to be pricing pressure.

Kraken sell other products – these are what you’ll see on the PNL historically. Most of these are poor barring AquaPix sonar. This is a sonar using a technology that produces much higher quality imagery than traditional sonar. It is sold with batteries to UUV customers though there is competition. Research suggests it is #1 quality sonar of this type, but pricing is relatively low inferring the gap to competing products is not that large.

Military UUVs are software defined. Anduril’s use Lattice as an operating system. Batteries are also software defined. Kraken’s battery management system (BMS) in a UUV controls power draw – used to regulate acoustic signature underwater. The UUV operating system and the BMS software’s must talk. During R&D testing Kraken builds an API in tandem with the customers operating system. In Anduril’s case the API is with Lattice and Kraken’s inhouse BMS.

This creates more headache upfront with architecture buildouts but makes the switching cost a lot higher for a customer.

Investment thesis: Pts #1 & #2 are discussed above.

Pricing power.

High switching costs.

Incoming orders

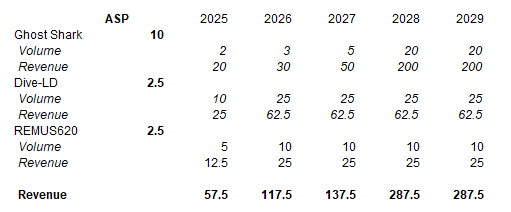

Kraken are sole source providers to Anduril’s Dive-LD and Ghost Shark UUV programs – both currently in R&D testing phase. ASPs are 10m/Ghost Shark and 2.5m/Dive-LD. They are also confirmed to supplying Konsberg’s REMUS class UUV.

Anduril and the Australian government collectively built a Ghost Shark manufacturing in 2024 to construct and test three initial prototypes. R&D testing “Mid-2025”. The first prototype was flown to the US for further R&D testing. If successful, Australia and the US defence forces are logical customers.

Upon receipt of R&D testing, Orders are likely placed 2025-2026 before a ramp in 2026-2027. Kraken expect 15-25 Ghost Sharks/pa. Taking the midpoint of 20 and ASP of $10m/per = $200m/pa revenue.

Dive-LD is a smaller UUV (~5m) It requires less batteries and hence ASP is lower at ~$2.5m. Anduril constructing a facility cable of producing 200/year. (At max capacity this 2.5x200 = $450m revenue/year in batteries)

Beyond Anduril, Remus, Konsberg HUGIN and Boeing Orca are all XLUUVs (extra large UUVs) currently in R&D testing – all potential battery customers.

(NB – batteries-specific revenue).

Risks

Capital intensity. Kraken are a manufacturer, currently building two additional facilities. EBITDA margins are likely capped at high 30’s with peak utilization. This, I am fine with. Specialized manufacturers make great businesses if they lack competition and have high switching costs.

Anduril Ghost Shark fails R&D testing. Based on conversations w/ management + orders already committed to Kraken (see announcements) this is extremely unlikely (<15%). What we know is that the US DoD will require a fleet of several hundred larger XLUUVs, which require higher energy density solutions relative to smaller drones – whichever XLUUV vendor is most successful be it, Konsberg, Boeing, HII, the end result is a fleet carrying Kraken batteries. There is downside protection in the case that Anduril, the most advanced offtake was to become delayed.

Valuation

Kraken can do ~$150m EBITDA on ~$400m revenue by 2029. On 15x EV/EBITDA, this is a ~$7.40 P/T. 143% upside & ~29% IRR.

Disclaimer:

The information contained in this post is for informational and entertainment purposes only and should not be construed as financial, investment, or other professional advice. I may hold or trade positions in the securities discussed, and such positions may change at any time without notice. All opinions expressed are solely my own, based on publicly available information, and do not constitute a recommendation to buy, sell, or hold any security.