Droneshield (DRO-AU)

What do I get for counter-drone tech @ 29x P/S?

Foreword

By reading beyond this introduction you agree to the disclaimer located in the footer of this post.

This will be a longform post hence the table of contents

Introduction

Cap table + SP history

Brief summary

History of incorporation

Overview of counter-drone market

Jamming vs. EW/kinetic

Financials

Balance sheet

Channel mix

Introduction

a) SP: $1.77, M/C: ~$1.6bn, EV: ~$1.4bn, ADV, ~$16m/day.

29x LTM P/S w/ 4% YoY sales growth.

Source - Crash Research

Source - Crash Research

1b)

Droneshield manufacture & market counter-drone products utilising jamming technology. Jamming is blasting the frequency on which drones/operaters use causing a disconnection + drone to stop working.

The company sell fixed site and mobile solutions with a tiny bit of software revenue on the side.

Source - Droneshield website

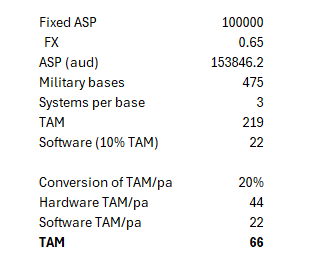

TAM is both defence and government.

Defence = in the field, army bases.

Civilian = Prisons, airports, stadiums

The FAA/FCC regulates non-governmental use of C-UAS in the US. The communications Act of 1934 stipulates that RF jamming/spoofing technologies are prohibited, as they interference with radio communications amongst other things.

You’ll find similar laws in Japan, Australia + many other markets.

As a result, the civilian TAM is small - the laws simply have not kept up with the tech.

Droneshield are in the game of selling (mostly) to defence customers, converting them as they adopt new counter-drone technologies.

Assuming US$100k ASP, 3x systems/base, a 5-year conversion period for ALL bases + some software revenue on the side gets you to a rough defence TAM of $66m/pa.

Source - Crash Research

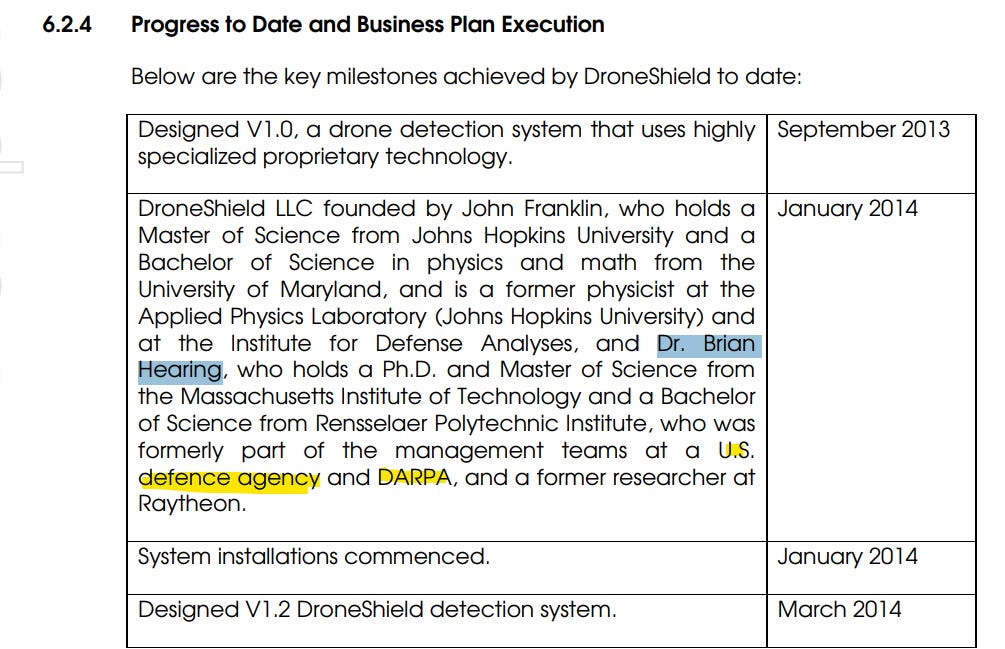

1c) History

Droneshield was co-founded by Brian Hearing and John Franklin before an IPO in 2016.

Source - Droneshield Prospectus

A Brian Hearing was prosecuted by the DOJ for “lying to federal investigators to conceal his ownership of a private company he was inappropriately using his official position to promote.”

Source - Justice.gov

Source - Droneshield Prospectus

Since then, Droneshield has grown revenues from <$1m to $58m, issuing it’s capital base ~8x to get there.

Overview of counter-drone TAM

2a) Counter-drone (C-UAS) is split into Kinetic (~50%), spoofing (~25%), jamming (~25%).

Kinetic refers to ballistic responses. e.g Cannons, lasers, missles to shoot down drones. e.g like EOS provide.

Spoofing is where drones can be remotely hacked into + controlled. Very technical stuff, at the bleeding edge of drone tech. e.g D-Fend Solutions

Jamming is Droneshield’s market - the fundamental of jamming is reliant on a known, non-moving communication channel between controller/drone that can be identified & severed.

In this instance, jamming is effective. Most civilian drones fall under this category. Stadiums/airports/prisons should be markets for jamming technology, except they currently aren’t because of legislation reasons.

Jamming is less effective against sophisticated military drones as the communication link is advanced or hidden. Many drones use ‘frequency-hopping’ where the radio frequency constantly moves meaning jamming devices cannot ‘lock-on’.

Other circumstances involve fibre-optic connections such as in Ukraine.

More advanced drones are pivoting to become pre-programmed or autonomous ‘AI-drones’ Where target coordinates are pre-empted, diminishing any communications between drone/controller.

Not only this, the top missle drones e.g Iranian Shahed’s travel at ~180km/h, meaning Droneshield fixed site systems w/ 1.5km range have ~30 seconds to detect the drone, figure out its frequency and jam it - unrealistic.

Jamming is at major risk of becoming a redundant in the defence space at the tradeoff of growth in electronic warefare and kinetic responses such as laser + microwave (see stocks $AVAV, $LASR, $EOS).

Financials

3a)

Droneshields financials are interesting and worth pointing out.

Inventory - a lot of CoGS are captialized on the balance sheet.

Like, a lot.

Inventory turn was 0.15x and days inventory climbed to ~1267 days (~3.5 yrs) in 2H’24.

Source - Crash Research

For a company with GPMs in the 70-80% range, this is worth noting.

Source - Crash Research

DroneShield margins are incidentally very strong for a hardware manufacturer that appears to have a lot of competition: DeDrone, WhiteFox, D-FEND, Fortem Technologies, Aerovironment, MyDefence, Skylock and so on….

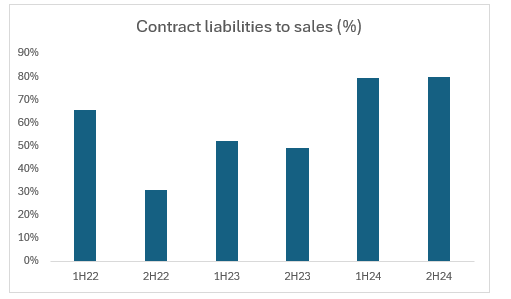

Contract liabilities - 80% of sales.

This is unusual for a manufacturer. They should be recognising revenue when goods are shipped.

Source - Crash Research

The notes to accounts suggest it is goods yet to be transferred.

Yet there are 1267 days of inventory - the company should have ample goods to ship. Perhaps it’s indicative of the timing of revenue recognition.

Days sales have climbed to 90 days.

The company suggests they should have 0-30 days. One can reasonably expect some down payments on orders, so 90 days seems elevated.

Source - Crash Research

There is a lot inventory, high margins and a lot of receivables (not many payments).

The reason: channel sales!(?)

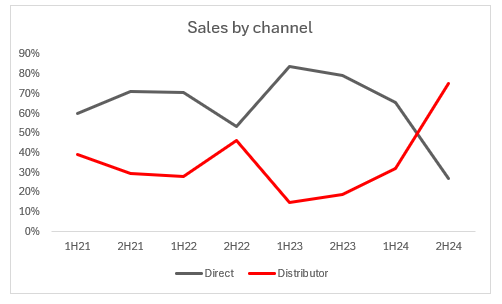

3b) Channel Mix

Droneshield sell both direct and via distribution channel, partially explaining why trade receivables balance is 3x as high as the supposed 30 day terms.

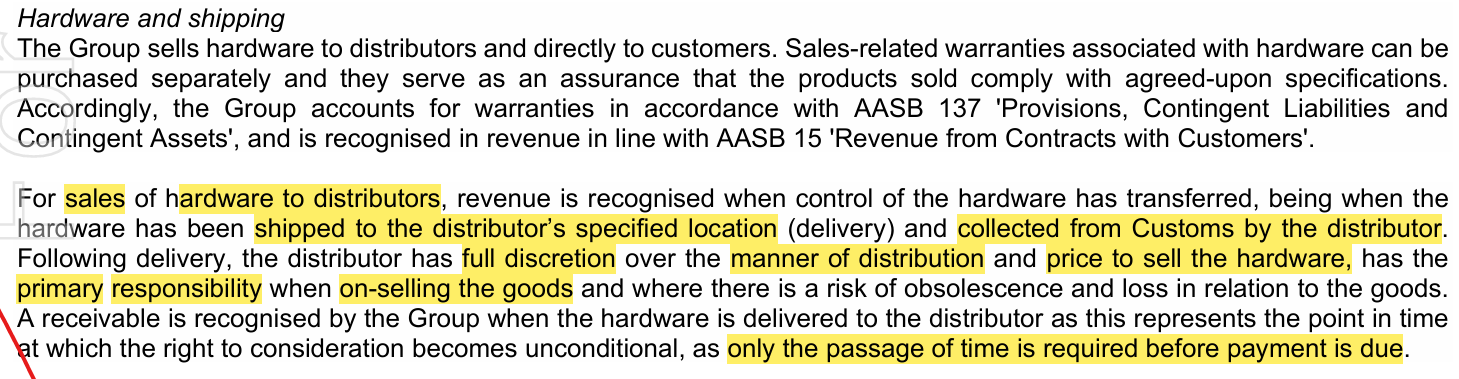

Hardware sales are recognised when goods are physically “shipped to the distributor’s specified location” AND "collected from customs by the distributor”

2024 saw a huge inflection in channel mix w/ a rise absolute rise in distributor sales seemingly at the expense of a collapse in direct sales.

Who are the distributors and why do they not appear to be paying Droneshield?

Droneshield does not disclose their distributers (frequently).

ForcePro B.V was a DroneShield distributor in the Benelux region. In 2020, Dronshield claims to have sold $100k to ForcePro.

Yet bankruptcy documents appear to show ForcePro having managed only €20k sales (A$30k) in 2020…

Not only that, but ForcePro had just two employees and not a whole lot of assets that one might reasonably expect to see for a partner of DroneShield, selling “multi-million dollar" of DroneGuns.

There is not much discussion in DroneShield about channel as a strategy. It’s worth highlighting the risks of selling defence weaponry (albetit, non-lethal) via a channel instead of direct - you lose control of which end customers are buying it.

Conclusion

At 29x LTM P/S the stock is dearly expensive.

In a peaking market full of competitors.

& the financials looks interesting to say the least.

Disclaimer:

The information contained in this post is for informational and entertainment purposes only and should not be construed as financial, investment, or other professional advice. I may hold or trade positions in the securities discussed, and such positions may change at any time without notice. All opinions expressed are solely my own, based on publicly available information, and do not constitute a recommendation to buy, sell, or hold any security.

Great article. You mentioned the weakness of jamming (might going obsolete), I also heard similar comments on jamming and this DRO versus EOS. what’s your view on DRO? Thanks

Are you long on DRO?